This is the main question we all have about our retirement future. How can we figure out what our future will be ? How long will we live? Should we base our life expectancy on how long our parents lived? Or perhaps our neighbors since we share a similar economic situation. A secure retirement means that we need to make an estimate of how long we will work, how long we will live and many other assumptions. In this post, we will discuss these issues and others that many consumers need to factor into their decisions.

This is the main question we all have about our retirement future. How can we figure out what our future will be ? How long will we live? Should we base our life expectancy on how long our parents lived? Or perhaps our neighbors since we share a similar economic situation. A secure retirement means that we need to make an estimate of how long we will work, how long we will live and many other assumptions. In this post, we will discuss these issues and others that many consumers need to factor into their decisions.

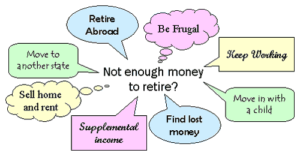

Will You Have a Secure Retirement

Are you already retired and wondering if you have enough to live comfortably during retirement? It is time to take stock of a number of things about your lifestyle and your situation. Here are a few, but the bottom line, your income must be the same or more than your expenses. Plus you need savings set aside for emergencies that invariably will come along.

Track expenses – to get an understanding of where your money is being spent. If you need to reduce, then you can start here and identify those areas where you can reduce and how much it will save you.

Track income – to understand how much is coming in and whether it will be enough or not. If not you may have to reduce expenses, go back to work, even if it is just part-time.

Re-evaluate every 6 months – life events and inflation happen all of the time. Recheck all of your calculations on a regular basis to make sure all of your assumptions are still accurate.

Balance income and expenses – as we said income must be higher than expenses otherwise it will eat into your savings quickly leaving you without enough to live on when you are much older.

Earn more, go back to work etc – going back to work can make a huge difference in both your life style as well as your savings. Your money will last much longer.

Reduce expenses

Do you really need to eat out all of the time? Can you make cost cutting painless. Look at all of your expenses and make a decision on those that can be reduced.

Downsize, rent, move in with the kids – if you must, these are drastic reductions that can be made to reduce your expenses.

Obtain expert help – find a financial advisor you can trust and review your situation with him or her. You may want to get several recommendations before settling on one direction or another.

For more retirement saving ideas, click here.