Does interest rate fluctuations mean that interest rates going up? One of the good things about the past recession or depression as some people would call it is that the interest we pay on loans and mortgages have been at historical lows. Many people would say this might be the only thing good thing about this recession. If you lost your job, or your home or have gone further in debt you probably are not interested in what is occurring with loan and mortgage interest rates.

Does interest rate fluctuations mean that interest rates going up? One of the good things about the past recession or depression as some people would call it is that the interest we pay on loans and mortgages have been at historical lows. Many people would say this might be the only thing good thing about this recession. If you lost your job, or your home or have gone further in debt you probably are not interested in what is occurring with loan and mortgage interest rates.

Interest Rate Fluctuations – Will they Change

However many of the worlds governments are letting their constituents know that interest rates are about to begin rising. How much and exactly when interest rates will begin to rise is not yet known, yet most informed sources feel that they will begin to rise in the second half of 2010. There are various strategies that one should consider depending on whether you are an investor or a borrower.

Note that any suggested advice we discuss in this blog is just that advice. We do not have a crystal ball and we really have no idea what will occur, however it is one writers opinion. Make your own assessment , read lots of material and make your own independent decisions.

Investor Strategies

If you are an informed investor, then you probably have a diverse investment portfolio with blue chip investments distributed among stocks, mutual funds and bonds across the various market sectors. That’s a big mouthful, however the message is do not ever put all of your eggs in one basket!

Typically when interest rates go up, existing bond values fall to maintain the overall yield, while new bonds being issued will have to offer higher interest rate yields to match the market interest rate. Dividend paying stocks also will decline so that overall yields will match the going interest rates on the market. Of course many other events can influence the value of the stock, such as corporate earnings and other market issues which will impact the overall value of the stocks value.

So what should you do when you see that the government is about to increase interest rates. If you are betting that the increases will be relatively minor, that they will not need to fight serious inflation, then you can take your time and be somewhat more careful about your plans.

Most people are long term investors, aiming at generating income and growth of their portfolios. With this in mind, fluctuations in interest rates and their corresponding impact are less troublesome. However there are some things you can do to make sure you take advantage of increasing interest rates and avoid the loss of income as interest rates decline.

Interest Rate Fluctuations – Bond Ladders

Creating a bond ladder allows you to invest in bonds with maturities over various years. For example if you have $100,000 , then investing $10,000 with a maturity in subsequent years lets you take advantage of bonds maturing every year instead of all at once when interest rates are low. You may not be able to invest all of your money at the highest interest rates, however your overall average will be higher than the lowest market interest rate.

As interest rates drop, you may find that bond lenders may call their bonds early. With this option, which many bonds have, the bond owners can pay off their bonds early. They issue new bonds at a much lower interest and save thousands of dollars. This is not a good situation for many investors who might be counting on this income. As you invest in bonds, always inquire whether the bond is callable or not and when. You will need to make your decision to purchase a callable bond, based on your assessment of where interest rates are headed.

We really like bond ladders with non callable bonds when interest rates are declining and especially when they are rising. We also like keeping approximately 5 to 10% of our portfolio in cash. If interest rates are headed up we can take advantage of the increasing rates. By cash we mean money markets or GICs with early maturity dates. You will not make much money, but every little bit counts. You will be ready when a good deal comes along.

What to do If you are Borrowing Money

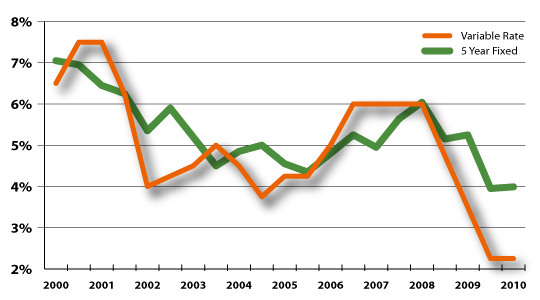

Interest rates are currently expected to rise. What should you do if you have a mortgage? Or a loan, or planning to borrow a large sum of money?

If you believe interest rates are going to rise significantly, it may be time to lock in your mortgage or loan so that you will not be hit by a financial shock when they do increase. You may find that there are hundreds of dollars added to your monthly payment when interest rates do rise.

If interest rates stay low for some time, you can actually save money by staying with an open mortgage. The interest rate will be tied to the bank rate. There is some risk to this approach because you could get caught if interest rates increase rapidly.

Bottom Line

If you are a risk taker, then you will take a more aggressive approach. You will be avoiding locking in your mortgage or loan for up to 5 years or more. On the other hand if you worry a lot or cannot withstand a financial shock, take a different approach. Locking in interest rates will protect you from fluctuations in monthly payments as interest rates change! At least you will not lie awake at night worrying about this issue.

Comments are welcome as are suggestions about what to do in this current situation.

Just looking at your site on my new Nokia Phone , and I wanted to see if it would allow me comment or if it made me go to a full pc to do that. Ill check back later to see if it worked.