We all tell ourselves lies from time to time. It makes life easier and we are able to get along with our lives. The problem is when we begin believing these lies and do not do something about the issues. But what about Lies We Tell Ourselves About Retirement Saving? We could find ourselves in serious trouble at some point. We may not achieve the retirement that we have always dreamed about. Our team summarized 5 lies we tell ourselves about retirement savings in an effort to help people identify these issues. they may be able to make the changes they need to make to ensure a comfortable and happy retirement. If you have dreams like the couple in this picture sitting on a sailboat or some other dream, pay attention and quit telling lies to yourself.

We all tell ourselves lies from time to time. It makes life easier and we are able to get along with our lives. The problem is when we begin believing these lies and do not do something about the issues. But what about Lies We Tell Ourselves About Retirement Saving? We could find ourselves in serious trouble at some point. We may not achieve the retirement that we have always dreamed about. Our team summarized 5 lies we tell ourselves about retirement savings in an effort to help people identify these issues. they may be able to make the changes they need to make to ensure a comfortable and happy retirement. If you have dreams like the couple in this picture sitting on a sailboat or some other dream, pay attention and quit telling lies to yourself.

5 Lies We Tell Ourselves About Retirement Saving

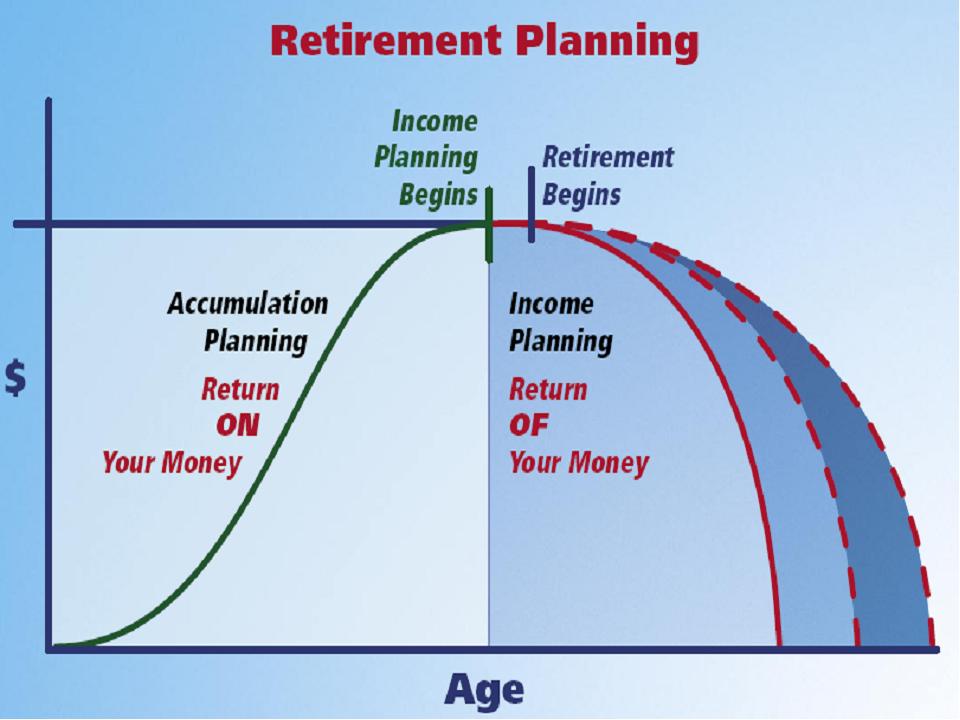

I have time to catch up on my savings. This is the biggest one that we all fall into. It is simple math to figure out how much money you need to save each month to achieve the level of savings that you will need in your retirement. Your financial adviser can help with these calculations. You will need to know how much income you need once you retire. What the sources of the income will be? Some will come from pensions and social security. The remainder needs to be generated from savings. How long will you save? How much can you save each month? What interest rate will you assume and how fast will you take out your money in retirement? Your adviser can help you with these assumptions and do the calculation for you.

I am going to die broke. But what happens if you live longer than you expected and now have to live in poverty? Can you predict when you will die? Even if you do not want to leave money for the kids, you still need to make sure you have sufficient funds to live out your life in comfort.

More Lies We Tell Ourselves

I will not linger. Maybe your parents did not linger, but with better health care, we are all living longer. Sometimes we live in spite of ourselves. When the time comes none of us really want to die.

Investment companies just want our money. Yes they want to make a profit, but they only make money over the long term if their clients are doing well. They get paid and they invest your money wisely. At the same time never blindly hand over your money to an adviser. Diversify your investments and get involved so that you know what is going on.

I will adjust to the income I have – easy to say but sometimes very difficult, especially if you must downsize your lifestyle. When we retire we have more time on our hands and that usually means that we spend more money too. Adjustment can be very difficult.