{kind=link}

This is always in addition to any fees that you might be paying your financial adviser to manage your overall account. These fees are charged to the mutual fund whether the manager has a good year or not. We have seen situations where the mutual fund has declined year over year and they still get paid their 2%. Almost like adding insult to injury in a situation like this.

Mutual funds are Expensive Compared to What

Consider that you will always be charged the expense fee regardless of how well your mutual fund actually does in any given year. Let’s assume that the investments your mutual fund is invested in provides a return of 5%, which is an aggressive return in today’s markets. We will leave that issue for another post. If your mutual fund and your investment adviser charge a combine 2% management fee, then your return on your mutual fund investment into your account will only be 3%.

Next consider, what happens in a down year. Lets say that investments do not do well and even though the investments in the mutual fund generate 5% income, the value of the stock portfolio declines and brings the net return into the negative territory. The MER is charged even though your fund loses money which adds to the overall loss.!

Mutual Fund Fees

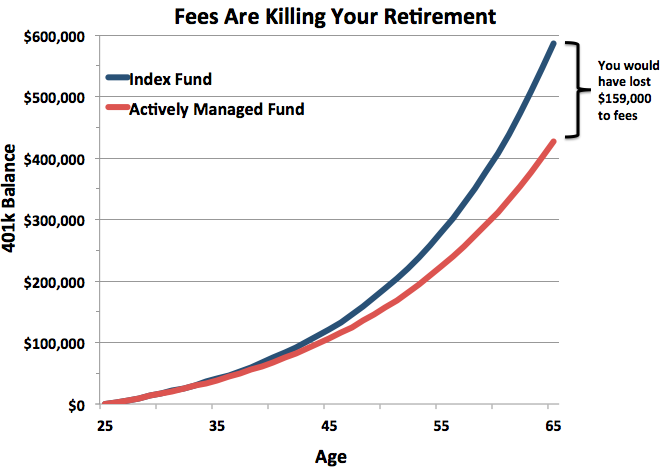

It is these fees that contribute to the $159,000 loss in the graph above. If you manage your own portfolio you can eliminate the management fees. You will still have some fees for trading but hopefully these will be kept to a minimum.

Since you have chosen blue chip stocks with a history of paying dividends each and every year.

Since you have high quality stocks there is also no need to rebalance. Or do a lot of trading each year which further decreases you overall fees.

Your fees can be significantly reduced leaving money in your account for your retirement. Something to think about!