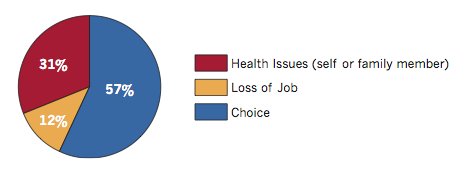

This is the big question for many people about to retire. What will they do in retirement? Will they be happy and what can retirees do if a retired lifestyle makes them unhappy? Sure there is lots of talk about being on the golf course every day, going for coffee with the gang and afternoons snoozing by the pool. Will this make them happy? Do they have enough money? What rewards to they get out of life? Do they have a purpose in life and what can they do about it?

This is the big question for many people about to retire. What will they do in retirement? Will they be happy and what can retirees do if a retired lifestyle makes them unhappy? Sure there is lots of talk about being on the golf course every day, going for coffee with the gang and afternoons snoozing by the pool. Will this make them happy? Do they have enough money? What rewards to they get out of life? Do they have a purpose in life and what can they do about it?

What can Retirees Do if a Retired Lifestyle Makes Them Unhappy

There is lots that retirees can do if they are unhappy. But first they need to figure out what makes them happy. Some need the regularity of going to work. Some need the friendships they obtain at work. For others, it is the challenge and the fear of the unknown. Will they make the deadline? Will they deliver on time. The adrenaline rush of success can be pretty sweet.

Many retirees keep themselves very busy. Busy hours fill the days and leaves them feeling that they have accomplished something. Whether it is looking after the grand kids, pursuing hobbies or improving their golf score, their days are full. They do not have time to wonder if they miss the challenges and the successes.

If you feel you have an unhappy retirement, it is time to do something about it. Start by reflecting on what is making you unhappy. Make a list if needed. Next determine what actions you can take that will positively change those items that make you unhappy. These might be broad brush strokes which you will need to refine in more detail.

Next make a plan. Decide how you will tackle the task and lay out the step by step approach to achieve your objectives. As will all projects there will be obstacles and detours along the way. They actually add to the challenge and make it even more interesting.

For more information about retirement surprises, click here.